Dama 2.0

In July 2024, LeafLink acquired Dama Financial from GrowFlow. Dama was a banking platform purpose-built for the cannabis industry. Cannabis is one of the few legal industries that traditional banks won't touch, and operators have spent years stitching together workarounds. Dama was meant to fix that, but the mobile app it came with was crashing on a daily basis, struggled to deposit checks, and had a 3/10 user rating to match. We rebuilt it from the ground up between Q4 2024 and Q2 2025.

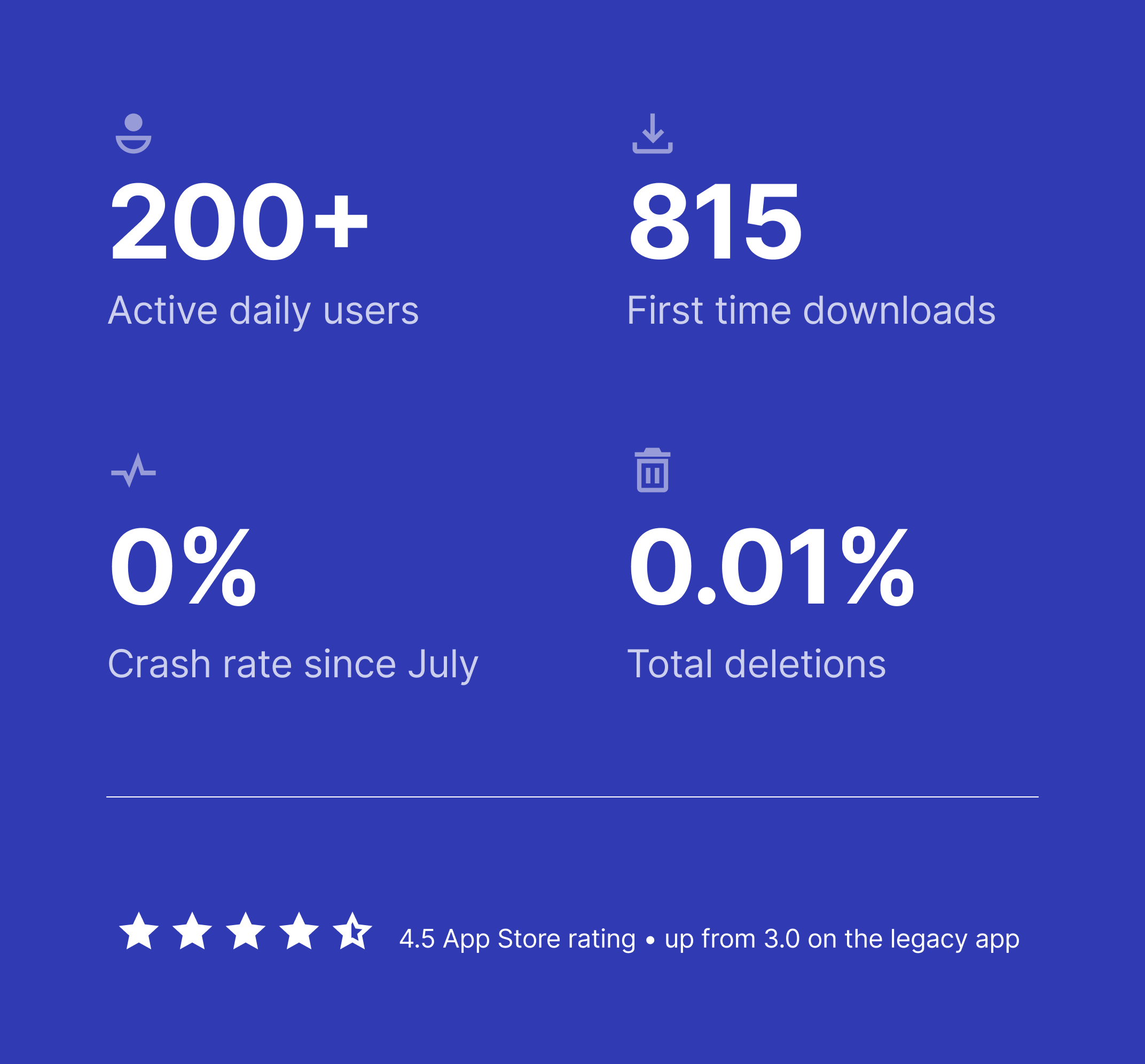

Since launch in spring 2025, the app has held a 0% crash rate, cut back-office touches on check deposits by 25%, and earned a 4.5-star rating in the App Store.

Dama Financial was acquired by LeafLink in July 2024.

Client: LeafLink - Dama Financial

Role: Design Lead

Year: October 2024 – May 2025

The case for buying instead of building

Before the acquisition, LeafLink had explored building a banking experience in-house. The blocker wasn't the design or the engineering. It was the time and complexity of standing up compliant banking partnerships and KYC infrastructure from scratch. For cannabis operators specifically, that means partnering with banks willing to work with the industry, integrating with fraud prevention vendors, and meeting regulatory requirements that change state by state. Years of work, easily.

The partnerships team identified Dama as the most viable path forward. Dama had spent years building exactly the relationships LeafLink would have had to construct on its own. Sponsor banks, FDIC-insured partners, fraud prevention infrastructure, payment processing rails. Acquiring Dama meant we could spend our time building a better experience on top of that foundation instead of recreating it.

The mobile app inherited from Dama needed real work. The UX was clunky, the hierarchy buried critical actions, navigation dead-ended, the IA was confused, and the UI was dated enough that customers had stopped trusting it. The bones beneath it. The partnerships, the compliance, the infrastructure. Were exactly what we needed.

Discovery

We started the rebuild by getting close to two groups of people: the internal teams who supported Dama every day, and the cannabis operators who used the app to run their businesses.

Internally, we ran 17 interviews across six departments: Sales, Client Services, Banking Operations, Compliance, Cash Operations, and Settlement Operations. The picture that emerged was consistent. Onboarding could take a month of hand-holding, document collection happened in side channels like Google Drive, the back office was manually reviewing 7,500 remote check deposits a month, and core operational work like updating partner permissions or moving money between systems involved copying and pasting between Salesforce, Shield (our third-party fraud vendor), and the app itself.

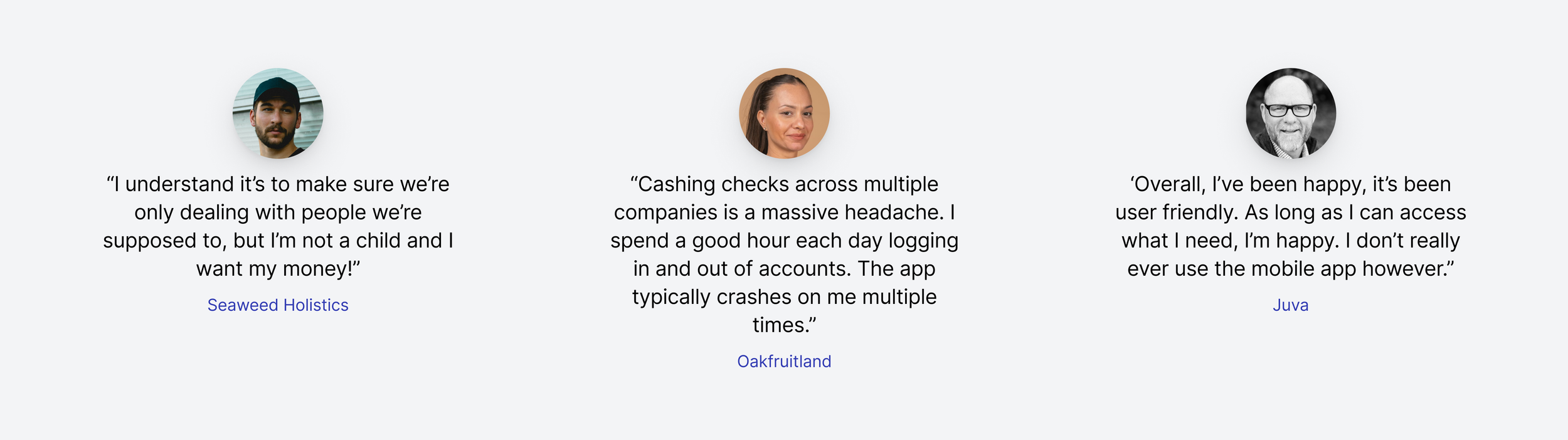

For customer research, we ran two trips to the San Francisco Bay Area in fall 2024 and met with ten cannabis operators of various sizes. The pain points were just as consistent on the customer side: check deposits failing up to five times before going through, app crashes that users had come to expect, 2FA failures locking people out, fragmented account access for operators running multiple legal entities, and confusion around courier and cash pickup services.

What we heard most often, in different forms: the app was a daily blocker for the people whose businesses depended on it.

Setting goals and looking outside

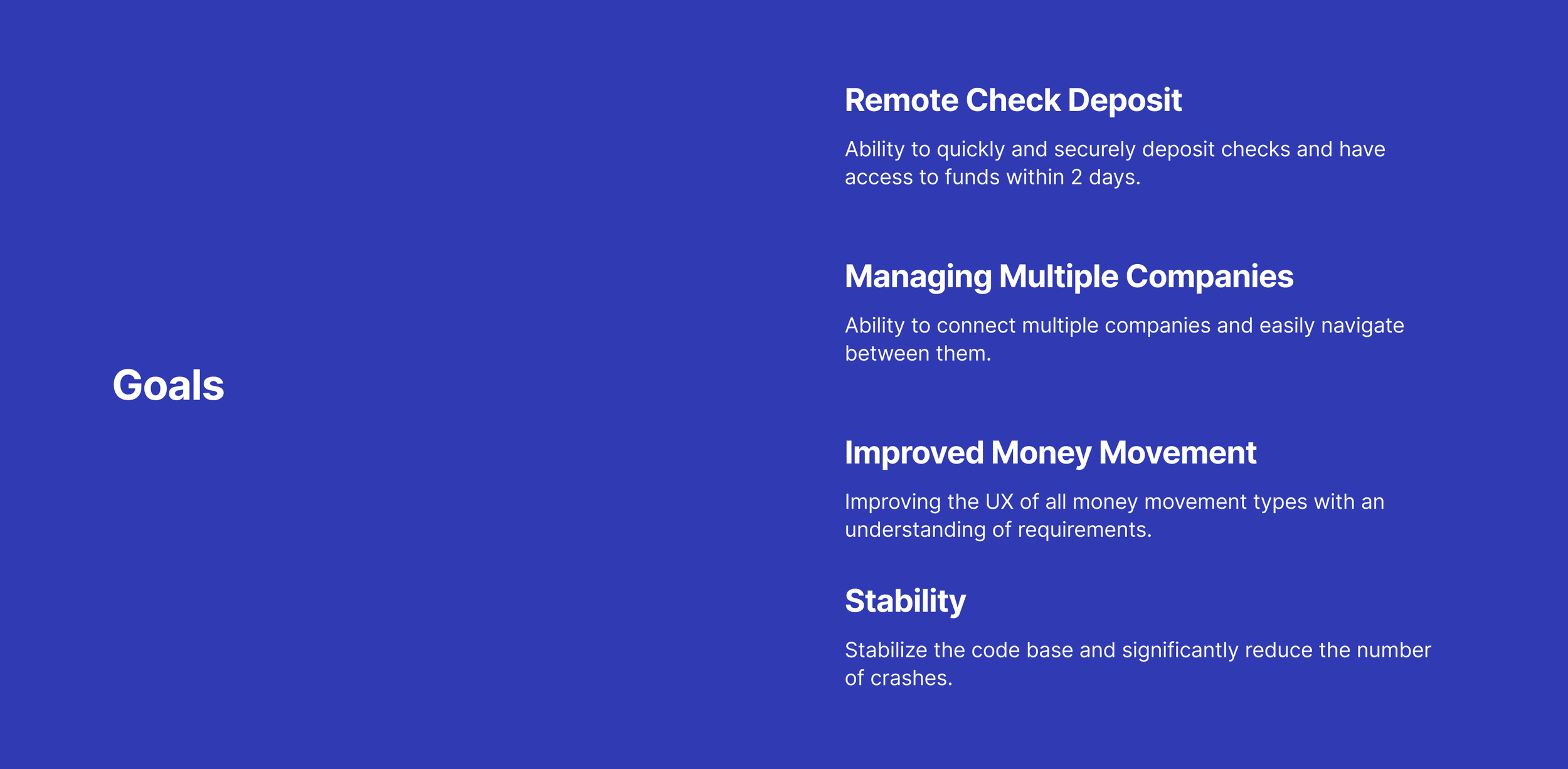

With discovery wrapped, we landed on four goals that would shape the rebuild: getting Remote Check Deposit to work reliably with funds available within two days, letting operators manage multiple companies from a single login, improving the UX of every money-movement flow, and stabilizing the codebase to drive crashes down.

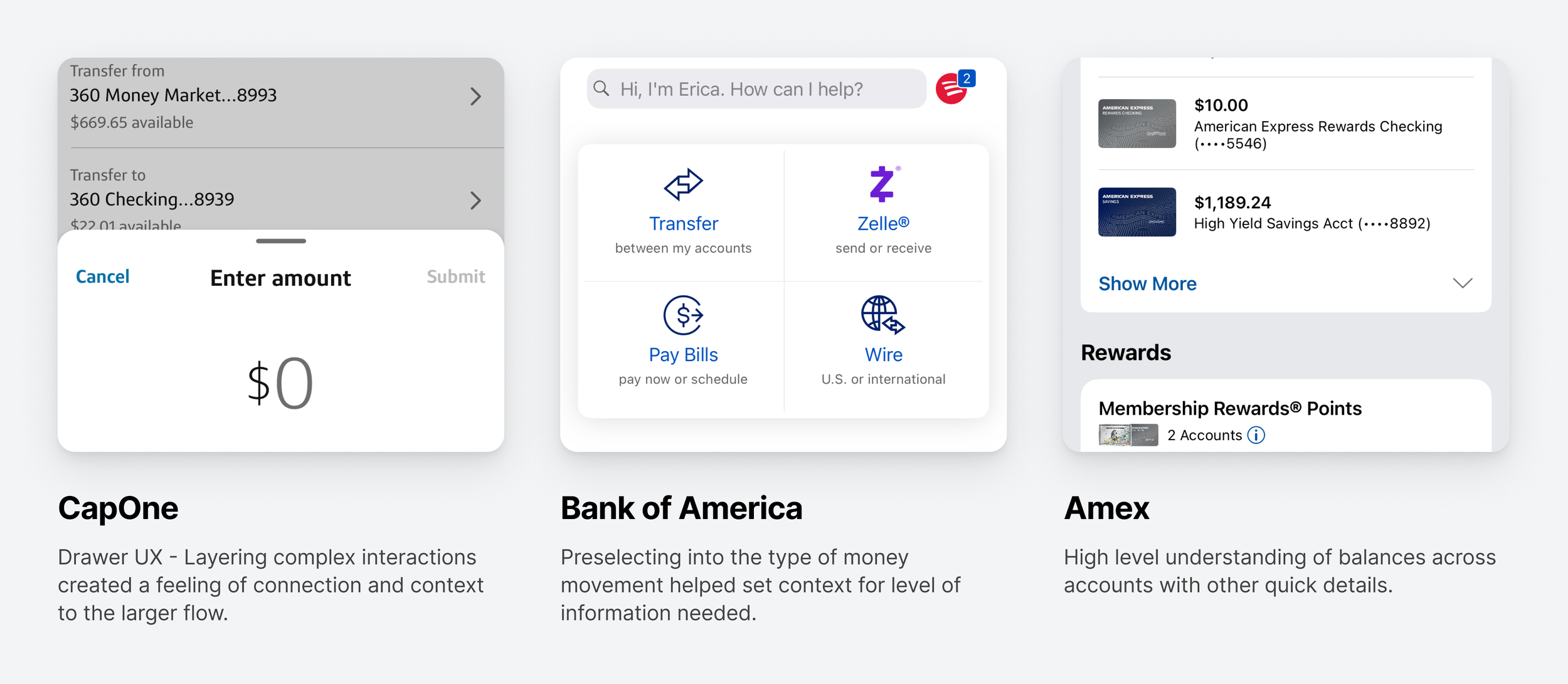

In parallel, we looked at how mainstream banking apps handled the patterns we needed to solve. Capital One's drawer UX showed how to layer complex interactions inside a single flow without losing context. Bank of America's home screen pre-selected money movement type before showing detail, which set a clearer mental model for users. Amex's account view gave a high-level read on balances across accounts at a glance. Exactly the kind of multi-entity visibility our customers had asked for.

Rebuilding the architecture

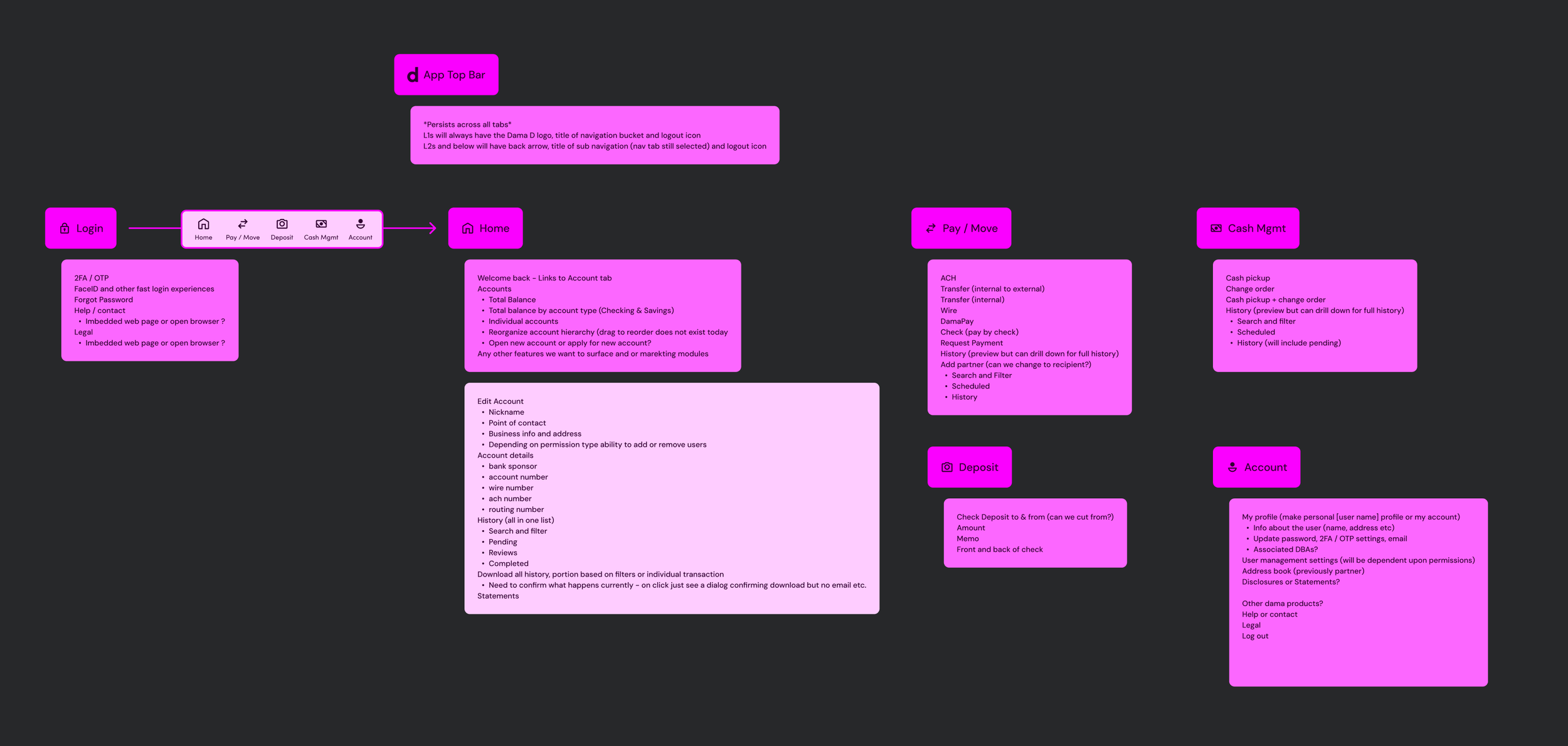

The original Dama app had grown the way most legacy apps grow: every new feature got bolted on wherever it could fit. The information architecture had become a sprawl that even the engineering team couldn't fully map without a reference doc.

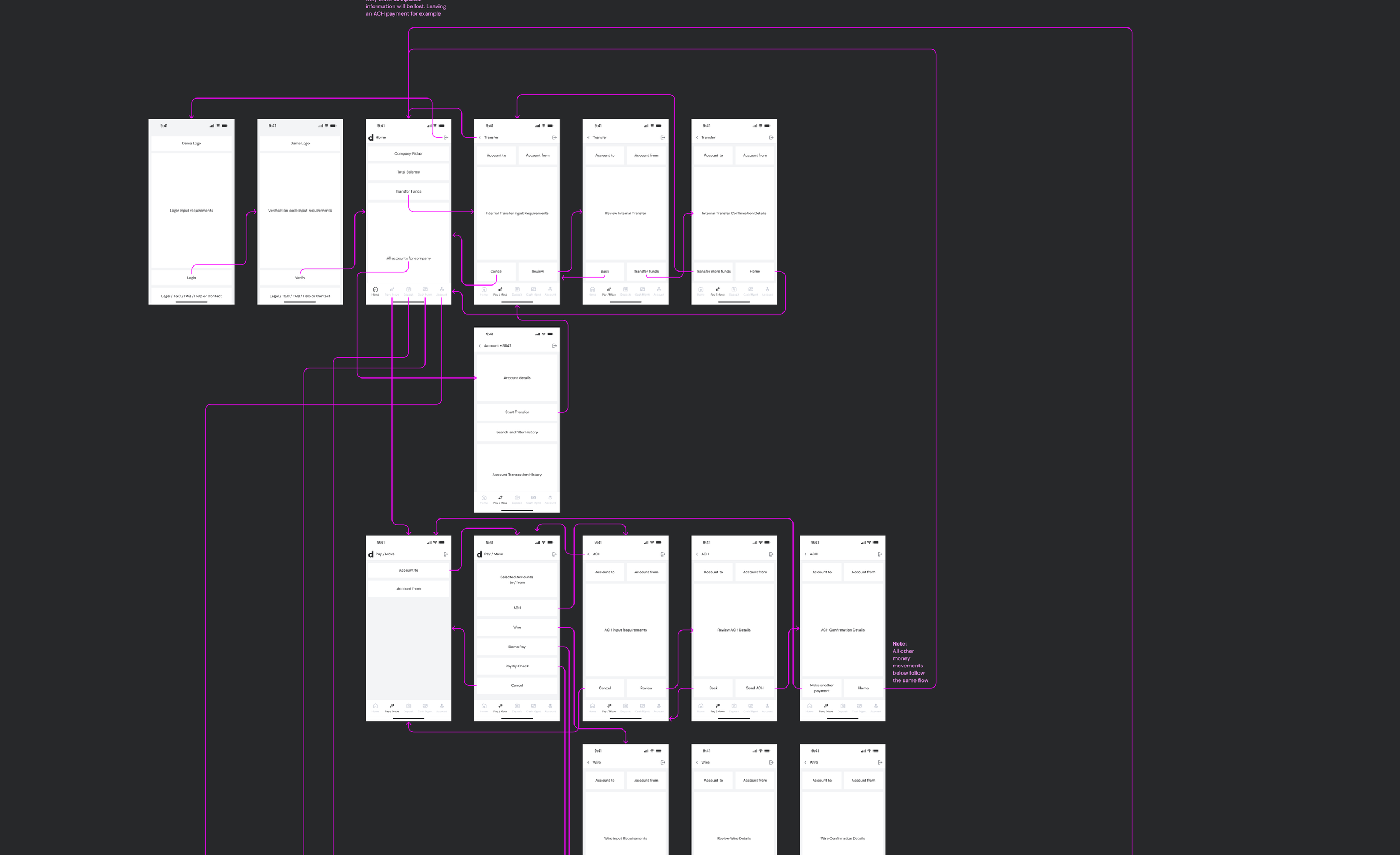

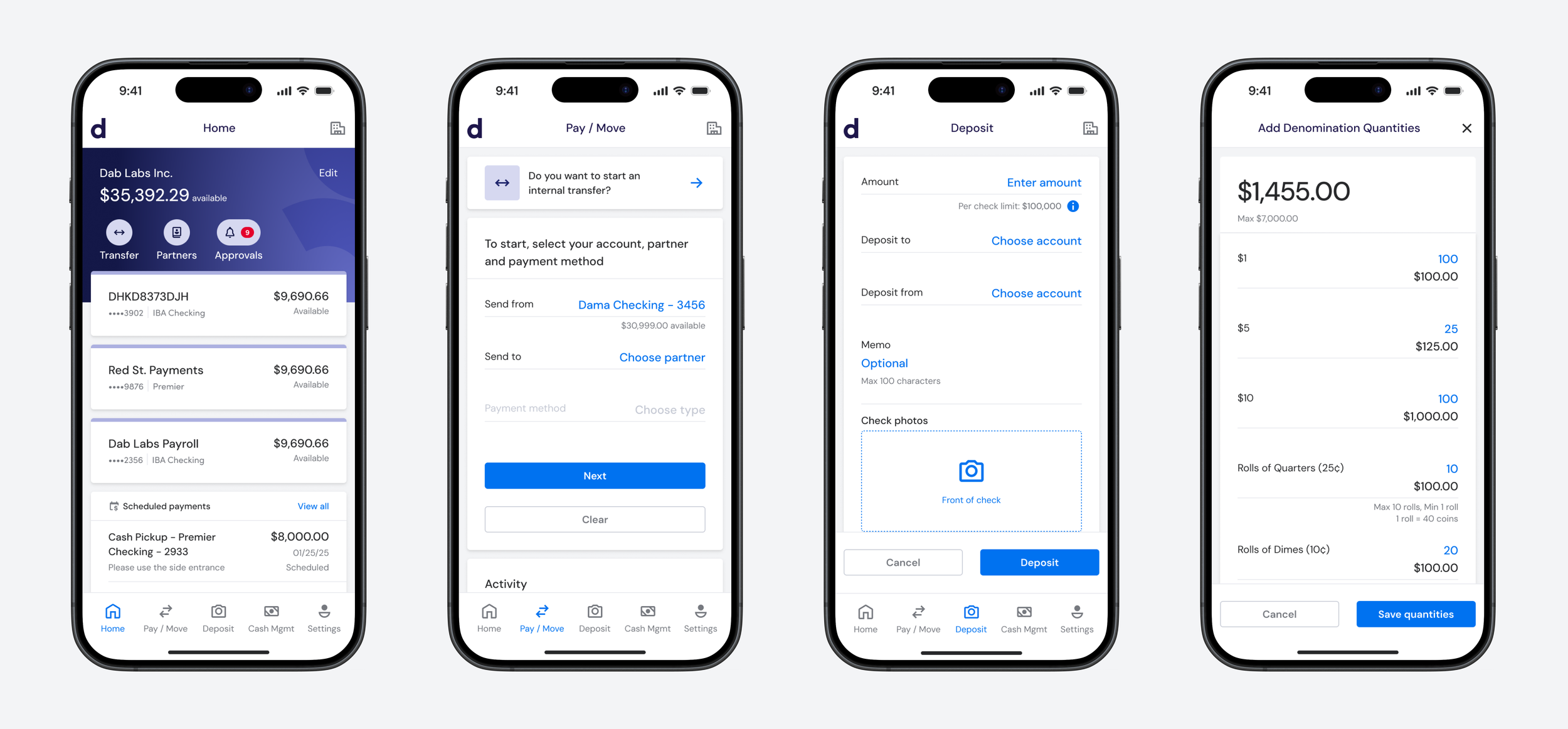

We rebuilt the IA from scratch around five primary surfaces: Home, Pay/Move, Deposit, Cash Management, and Account. Each one had a clear job, and every flow inside the app could be traced back to one of them. The new structure also gave us a place to land features that had been homeless in the old app. Things like multi-company switching and pending approvals. Without forcing them into navigation slots they didn't belong in.

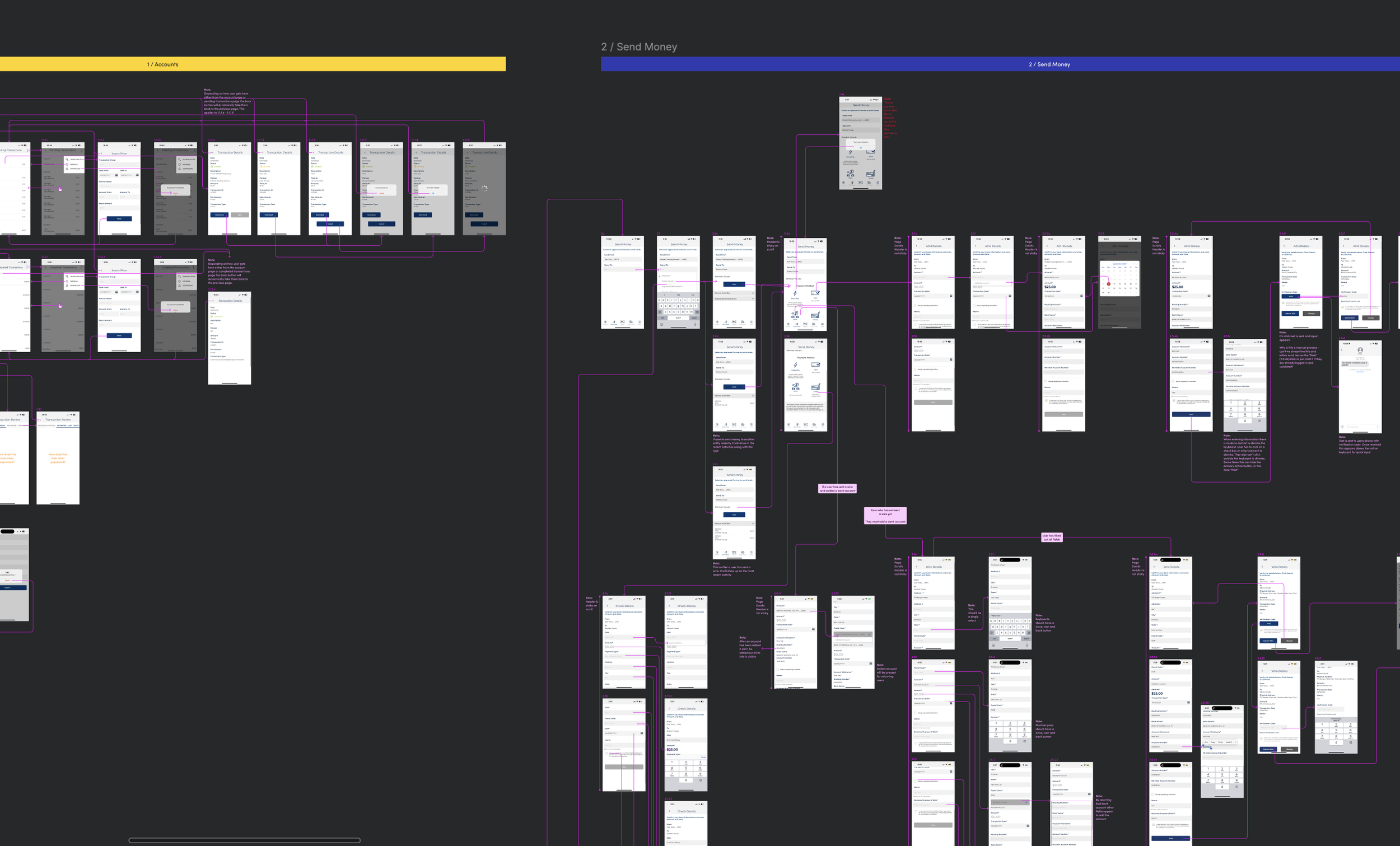

From there we built out wireframes for the new flows, anchored on what the discovery research had told us mattered most: getting deposits to work, navigating between companies, and moving money confidently.

Extending the system into mobile

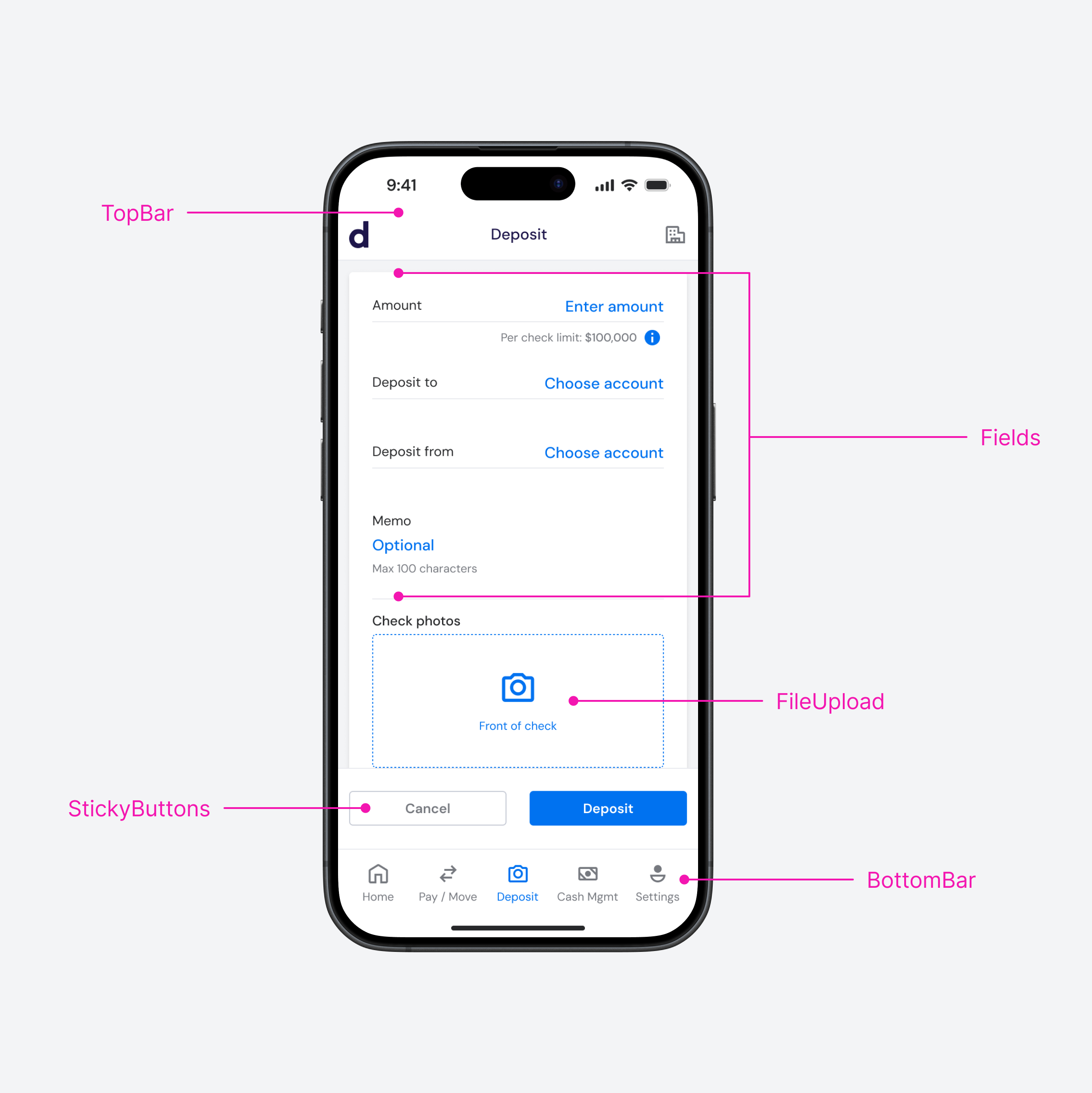

Stash, LeafLink's design system, had been built for the web. To bring its consistency into a native mobile app, we ran a parallel monorepo effort to decouple Stash from any single codebase. That gave us the freedom to build natively in React Native while still pulling from Stash styles directly. Same colors, same typography, same component logic, just rendered for mobile.

Once the foundation was in place, we extended the system mobile-first across every component the app needed: top bars, bottom navigation, fields, file uploads, sticky action buttons. The mobile app ended up looking and feeling like part of the LeafLink product family. That mattered because operators were going to be moving between LeafLink's wholesale platform and Dama's banking app daily.

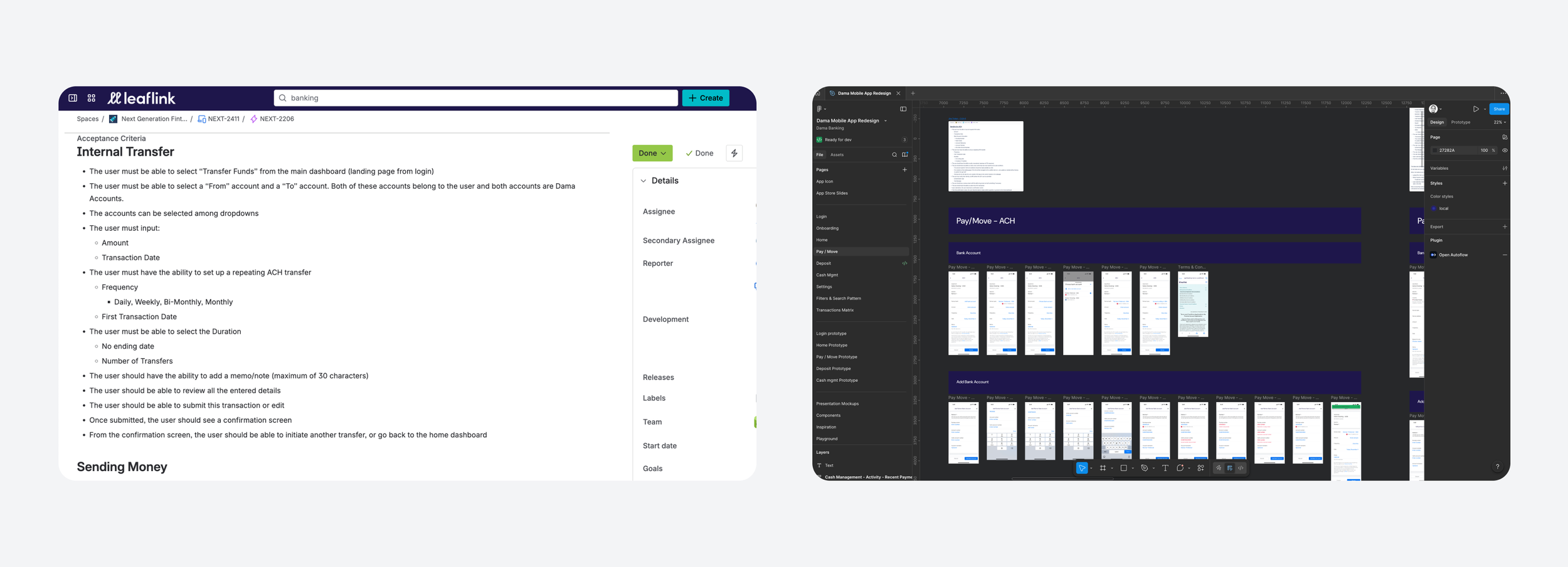

The build itself ran tight. I worked roughly two sprints ahead of engineering, maintaining feature-level documentation linked to Jira tickets so PM, design, and engineering could move in lockstep without bottlenecking on me.

Left - Feature Area Epics | Right - Organized in Figma

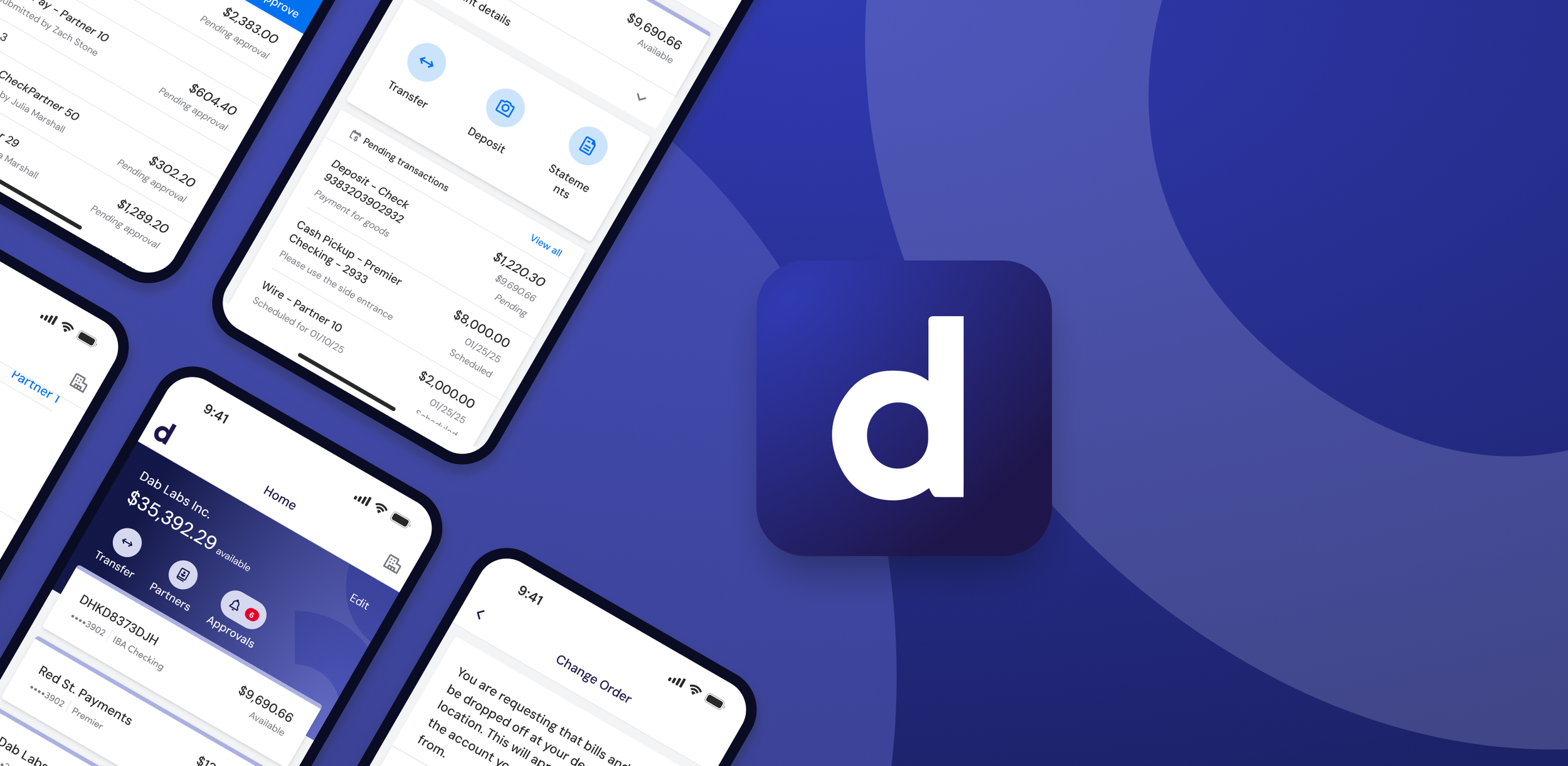

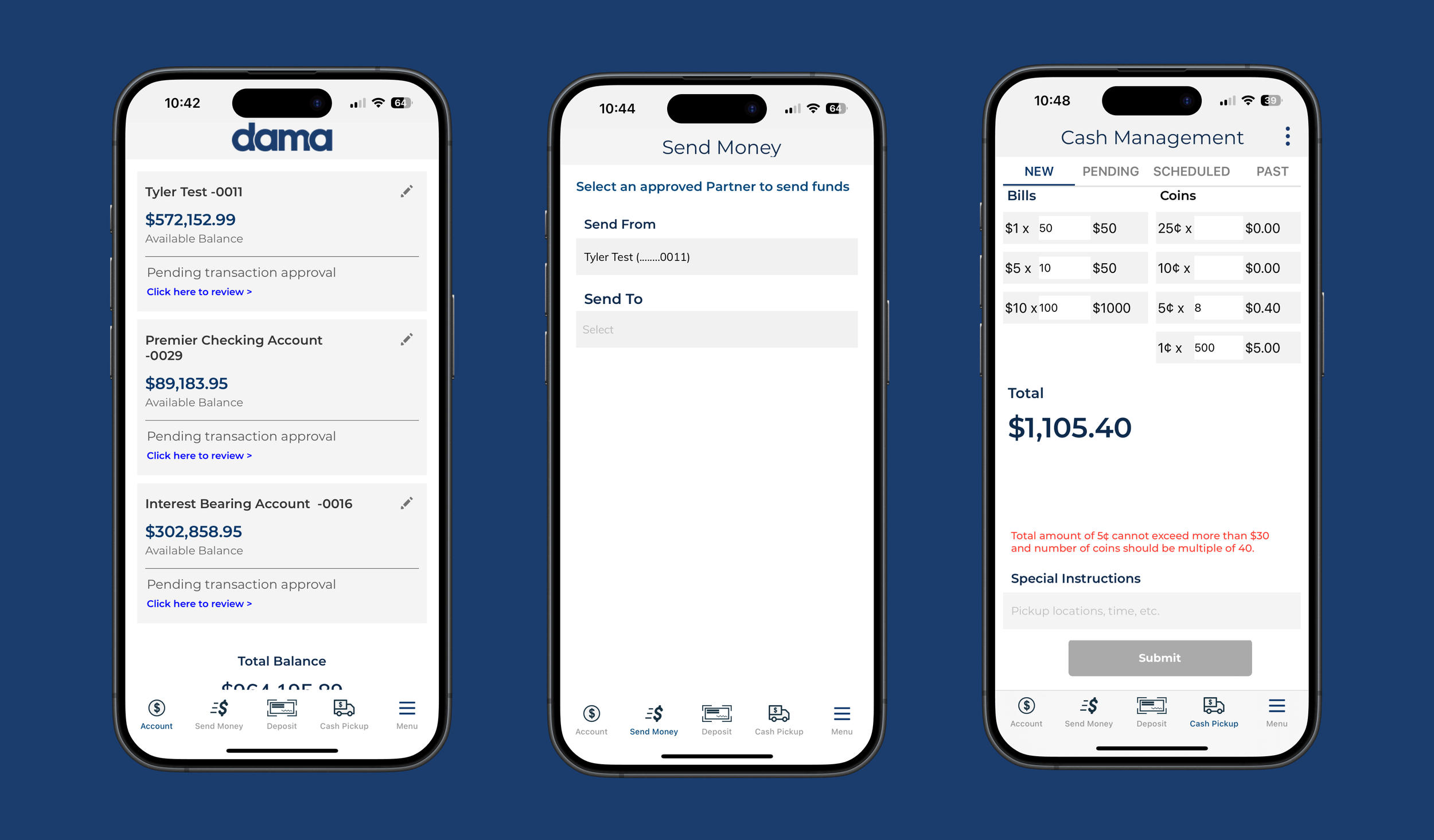

The redesigned app

Five primary surfaces, all sitting on top of the rebuilt IA, the extended Stash mobile system, and the partnerships and infrastructure that came with the acquisition.

The Home screen anchors a multi-account view with quick access to transfers, partners, and pending approvals. Pay/Move walks operators through a single guided flow regardless of payment method: ACH, wire, internal transfer, or partner payment. Deposit handles remote check capture with clear per-check limits surfaced before the user gets to the camera. Cash Management gives operators direct control over scheduled cash pickups and change orders, which had been buried in the legacy app.

Outcomes

We launched the rebuilt app to a closed beta in spring 2025 and opened it up to general availability in June. The numbers since launch:

Beyond the App Store data, the back office saw a 25% reduction in manual touches on remote check deposits, measured against the same 7,500-per-month baseline that surfaced during the audit. Customers also reported preferring mobile to desktop for daily operational work. A reversal from the legacy app, which they avoided on phones.

Looking back

The two things I'm proudest of weren't the headline outcomes. The check capture flow held up at scale because we tested it harder than anything else in the app, and the back-office reduction is the evidence. The team held up too. Building a banking app from audit to GA inside seven months meant every member picked up work outside their lane to keep the launch on track.

What I'd do differently: more time on UI exploration. Some of the UX improvements we'd hoped to deliver got deferred until the underlying databases were rebuilt. Better search, clearer pending-transaction visibility, smarter notifications. The system we extended into mobile carried us, and I'm proud of how it held up. With a longer runway I would have pushed the visual language further into the new space.